For many small businesses, growth eventually requires outside funding. Maybe you need working capital, want to purchase heavy equipment, or plan to invest in commercial real estate. SBA backed loans are often one of the most accessible paths to financing.

Still, the range of options can feel confusing at first. An SBA 7a vs 504 vs microloan comparison helps small business owners understand the key differences between programs and choose the right loan option for their goals.

Key Takeaways

-

SBA loans provide several financing options designed for different business purposes.

-

A clear SBA loan comparison helps determine whether a 7(a), 504, or microloan program fits your needs.

-

SBA 7(a) loans offer flexible funding for working capital, acquisitions, and debt refinancing.

-

SBA 504 loans focus on acquiring fixed assets such as real estate or heavy equipment.

-

Microloans provide smaller funding amounts for startups or early-stage companies.

Why SBA Loans Exist

The Small Business Administration supports small businesses by guaranteeing a portion of loans issued by qualified lenders. This reduces lender risk and encourages banks to offer long term credit to businesses that might otherwise struggle to secure financing.

These programs allow entrepreneurs to access capital with competitive interest rates, lower down payments, and structured loan terms designed for sustainable growth, similar to the educational resources highlighted on our small business and banking insights blog.

To qualify for most SBA programs, a company must operate as a for-profit business in the United States and meet eligibility requirements based on size standards. Lenders evaluate personal credit, collateral requirements, and the company’s ability to repay the loan.

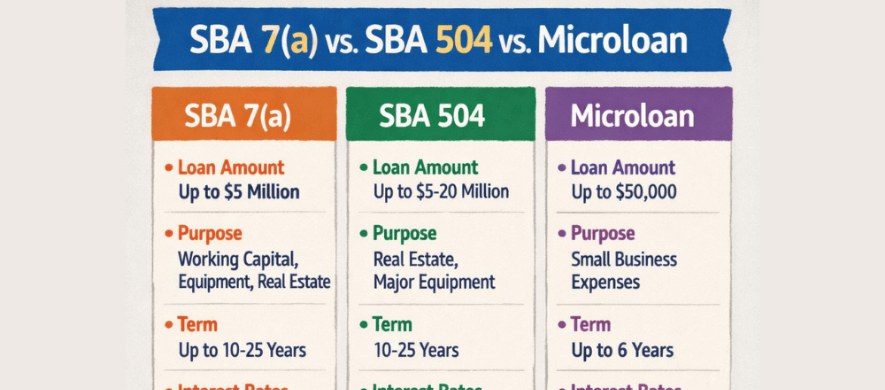

SBA 7(a) Loans: Flexible Funding for Many Business Needs

Among all SBA loan programs, the 7(a) loan program is the most widely used. These loans provide flexible financing for a wide range of business purposes.

A 7 a loan can be used for:

-

Working capital

-

Inventory purchases

-

Equipment financing

-

Debt refinancing or refinancing existing debt

-

Business acquisitions

-

Commercial real estate

The maximum loan amount for SBA 7 a loans can exceed $5 million, making the program suitable for both small and mid-sized companies. Borrowers may choose fixed or variable interest rates depending on their financial strategy. Many lenders link variable rates to the current prime rate.

Because these loans can support everyday business operations and address cash flow challenges, they are often the most versatile SBA loan type, especially when paired with tools like business credit cards for managing ongoing expenses.

Collateral requirements vary depending on the loan amount. For example, loans under $25,000 may not require collateral, while loans greater than $350,000 typically require lenders to secure assets to the maximum extent possible.

SBA 504 Loans: Designed for Fixed Asset Investments

While the 7(a) program offers broad flexibility, the SBA 504 loan program focuses on fixed asset purchases that support long term business growth.

A 504 loan can finance:

-

Commercial real estate

-

Construction projects

-

Facility expansion

-

Heavy equipment purchases

-

Other fixed assets tied to operations

The structure of an SBA 504 loan is unique. It involves three parties: the borrower, a conventional lender, and a Certified Development Company. These loans typically provide fixed interest rates for the CDC portion of the financing, which helps business owners predict payments over time and control overall financing costs.

The program generally requires a down payment between 10% and 20%. Eligibility also includes financial limits such as a tangible net worth below $20 million and average net income under $6.5 million. Unlike the 7(a) program, 504 funds cannot be used for working capital or debt refinancing.

SBA Microloans: Smaller Funding for Early Growth

Not every business needs millions of dollars in financing. Startups and smaller companies may only need modest capital to move forward.

That is where SBA microloans come in. Microloans are administered through nonprofit intermediary lenders instead of traditional banks. These organizations often provide mentorship and training along with funding.

Microloans typically support:

-

Startup expenses

-

Inventory purchases

-

Equipment or technology upgrades

-

Short term operating costs

Loan amounts generally reach up to $50,000, making this program especially useful for early stage companies. Interest rates are usually fixed and commonly range between 8% and 13%. Because credit standards are often more flexible, microloans can be a practical first step for entrepreneurs launching a new venture that may later benefit from business loans that support innovation and expansion.

Comparing Key Differences Between SBA Programs

Understanding the key differences between programs helps business owners make an informed decision.

7(a) loans

-

Flexible funding for many business purposes

-

Can be used for working capital, acquisitions, and debt refinancing

-

Maximum loan amount may exceed $5 million

-

Offered through SBA approved lenders

504 loans

-

Designed for fixed asset purchases

-

Often used for commercial real estate or equipment

-

Fixed interest rates on CDC portion

-

Encourages long term business growth and job creation

Microloans

-

Smaller funding amounts for startups or small operations

-

Issued by nonprofit intermediary lenders

-

Faster application process with training support

Each loan type offers unique benefits depending on the company’s needs.

Finding the Right Financing Partner

Understanding the differences between SBA programs is only the first step. The application process still requires preparation.

Lenders typically evaluate financial statements, credit history, and business plans before approving SBA-backed loans. A strong financial foundation and clear strategy help streamline the process.

Choosing the right financing partner matters as well. Experienced lenders that specialize in commercial loans and business lines of credit understand the nuances of SBA programs and can help guide applicants through documentation and approval requirements.

Moving Forward With Your SBA Loan Decision

Every SBA loan program serves a different purpose. The best option depends on how your business plans to grow.

A thoughtful SBA loan comparison allows business owners to match the right financing tool to their goals. Whether you are expanding operations, purchasing property, or launching a startup, understanding these programs helps you approach funding with greater confidence.

At Farmers Bank, our experienced lenders work closely with local entrepreneurs to navigate SBA loan options and guide them through the application process. If you are exploring financing for your business, contact Farmers Bank today to discuss the best loan program for your next stage of growth.

FAQs

What is the difference between 7(a), 504, and microloan programs?

7(a) loans offer flexible financing for many business purposes, while 504 loans focus on acquiring fixed assets such as real estate or equipment. Microloans provide smaller funding amounts designed for startups or small businesses.

What can SBA 7(a) loans be used for?

These loans can fund working capital, equipment purchases, acquisitions, inventory, or debt refinancing.

Are SBA 504 loans only for real estate?

Not exclusively. While commercial real estate is common, the program can also finance major equipment or other fixed asset investments that support business expansion.

Who provides SBA microloans?

Microloans are typically administered through nonprofit intermediary lenders that partner with the Small Business Administration.

How long does it take to get approved for an SBA loan?

Approval timelines vary depending on the loan type and documentation provided. Some 7(a) loans may be processed within a few days, while larger 504 loans often take longer due to their multi-party structure.