1/23/2026

Small Business Loans & Financing in Idaho

Idaho is home to a thriving network of small businesses, each with unique goals, industries, and stories. Whether you're seeking startup funding, need to manage cash flow during a slow season, or are ready to scale operations, the right loan can make a major impact. At Farmers Bank, we offer tailored loan products with competitive interest rates and personalized support, delivered by people who understand the needs of Idaho business owners.

1/23/2026

Mobile and Online Banking Services in Idaho Customers

Managing your finances shouldn't feel like a chore. Whether you're a busy parent in Twin Falls, a small business owner in Wendell, or just someone who wants more control over their day-to-day banking, Farmers Bank offers online banking services in Idaho that are secure, flexible, and designed for convenience. With our mobile banking app, you can access your bank account on your schedule, not the bank's.

2/23/2026

Idaho First-Time Home Buyer Programs: 2026 Guide

Buying your first home is a milestone worth celebrating, but getting there takes more than just excitement. In Idaho, there are several programs designed to help ease the financial pressure that often comes with a home purchase. From payment assistance to FHA loans and tax deductions, knowing your options can help you plan with confidence.

2/23/2026

HELOC vs Home Equity Loan: Which Is Right for You?

When you’ve built up equity in your home, it can become a valuable tool for achieving financial goals; whether you're funding a renovation, consolidating debt, or covering major expenses. But choosing between a home equity loan or a home equity line of credit (HELOC) isn’t always straightforward. These options both fall under the umbrella of second mortgage loans, and while they tap into the value of your home, their structure, flexibility, and repayment terms differ in meaningful ways.

2/23/2026

Smart Ways to Prepare Credit for Mortgage Approval

Buying a home is one of the most exciting milestones in life but it’s also one of the most financially significant. If you’re planning to apply for a mortgage, your credit profile plays a key role in determining your eligibility and the loan terms you receive. The better your credit health, the better your chances of qualifying for a favorable rate and smoother approval process.

3/3/2026

When Should You Refinance Your Mortgage?

Refinancing sounds simple on the surface. Swap out your current mortgage for a new loan, hopefully with better terms. But knowing when to refinance mortgage decisions make financial sense takes more than watching headlines.

3/3/2026

What Is PMI and How Can You Remove It?

You review your monthly mortgage payment and notice a line item labeled PMI. It raises a fair question: what is PMI, and why are you paying it?

For many homeowners, private mortgage insurance shows up during the homebuying process when a smaller down payment makes sense. The key is understanding how it works and knowing when you can remove PMI.

4/2/2026

SBA Loan Requirements: How to Qualify

Access to capital can be the difference between steady growth and stalled progress for many small businesses. Whether you need working capital, equipment, or funding for expansion, SBA backed financing programs often provide flexible terms that traditional lending options may not offer.

4/2/2026

Writing a Business Plan for SBA Financing

Every successful company starts with an idea. Turning that idea into a funded, operating business usually requires capital. For many small business owners, SBA financing provides an accessible path to funding through trusted lenders.

Read Post

4/2/2026

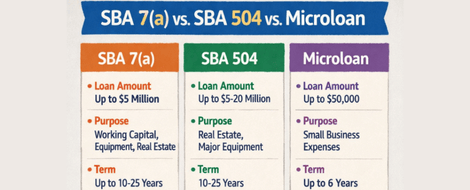

SBA 7(a) vs 504 vs Microloans: Choosing the Right SBA Loan

For many small businesses, growth eventually requires outside funding. Maybe you need working capital, want to purchase heavy equipment, or plan to invest in commercial real estate. SBA backed loans are often one of the most accessible paths to financing.

5/12/2026

Cash Flow Management Tips for Small Businesses

Cash flow can feel unpredictable at times. One month looks strong, the next feels tight, even when revenue appears steady. That tension is common for small business owners, and it often comes down to how money moves through the business.

5/12/2026

Resources for New Farmers: Complete Guide

Starting a farm takes more than land and equipment. It takes planning, access to capital, and the right support system. For beginning farmers, knowing where to find reliable guidance and funding can make a meaningful difference early on.

Read Post

6/1/2026

Idaho Business Success Stories: Growing with Local Support

Every successful business has a story behind it. Not always flashy. Not always headline-worthy. Sometimes it’s steady growth, smart decisions, and the right support at the right time.

6/1/2026

Managing Seasonal Cash Flow in Agriculture

Cash flow in agriculture rarely follows a straight line. Income tends to arrive in waves tied to harvest or livestock sales, while expenses show up steadily and sometimes all at once. That imbalance can create pressure, even for a profitable farm business.

7/1/2026

Financing Renewable Energy Projects on Farms

Energy costs affect nearly every part of agricultural production. Irrigation systems, refrigeration equipment, grain storage, ventilation, and processing facilities all require reliable power, and those expenses can add up quickly over time.

7/1/2026

FDIC Insurance Coverage Explained

Most people have heard the phrase “FDIC insured,” but many are still unsure what that protection actually covers. Questions about bank deposits, insurance coverage, and financial stability often become more common during periods of economic uncertainty or after major headlines involving failed banks.

7/1/2026

How to Build an Emergency Fund

Unexpected expenses have a way of showing up at the worst possible times. A major vehicle repair, a medical bill, a broken appliance, or even a temporary loss of income can quickly disrupt your financial situation if you are not prepared.

Additional Articles:

January:

February:

-

Idaho First-Time Home Buyer Programs: 2026 Guide

-

HELOC vs Home Equity Loan: Which Is Right for You?

-

Smart Ways to Prepare Credit for Mortgage Approval

March:

April:

June:

-

Idaho Business Success Stories: Growing with Local Support

-

Managing Seasonal Cash Flow in Agriculture

12/1/2025

Home Equity Loans vs Home Mortgages: What’s Best for You?

When tapping into the value of your home, there are two major routes to consider: taking out a mortgage or using home equity. Both options can support major life goals like home improvements, debt consolidation, or securing long-term stability; but they operate differently, and the right choice depends on your financial situation.

12/1/2025

How to Leverage SBA Loans for Business Growth

Sustainable growth rarely happens by accident. It takes planning, persistence, and the right funding strategy. For small businesses looking to move from surviving to thriving, SBA loans offer a bridge to greater opportunity. These government-backed loan programs open the door to flexible, affordable financing options that can be applied across a variety of business purposes.

11/1/2025

Empowering Innovations with Business Loans

Small business owners know that innovation isn’t just a buzzword, it’s the fuel that drives long-term success. Whether you’re ready to invest in new tech, bring a fresh idea to market, or fund your next big move, business loans offer more than financial support; they unlock the momentum your growth needs.

11/01/2025

Overcoming Financial Challenges with Ready Reserve

Life has a knack for throwing surprises your way, some exciting, others expensive. Whether it’s an unexpected car repair, a medical bill, or simply forgetting an automatic subscription charge, these financial hiccups can be stressful. That’s where Farmers Bank’s Ready Reserve line of credit comes in.

.png)

10/1/2025

Personalizing Your Banking Experience with Farmer’s Bank’s MyCardCreation®

Banking is personal. From the way you manage your finances to how you interact with your bank, every detail should reflect your preferences. With Farmers Bank’s MyCardCreation® service, even your debit card can be a direct expression of your personality, business, or lifestyle. It's more than just plastic in your wallet; it’s a custom tool designed to reflect you, and it’s completely free.

%20(16).png)

10/1/2025

Unlocking Opportunities: The Power of Commercial Real Estate Loans

When businesses start to outgrow their current space or look toward expanding operations, real estate becomes a major part of the equation. Owning commercial property offers control, potential tax benefits, and a reliable way to build equity. But purchasing or developing that property takes the right kind of financial support; namely, a commercial real estate loan that’s tailored to your goals and growth strategy.

%20(15).png)

10/1/2025

Navigating Auto Loans with Farmers Bank: A Local Approach to Vehicle Financing

When it comes to buying a car, your financing experience should feel just as smooth as the open road ahead. That’s why more Idaho drivers turn to Farmers Bank for auto loans that are grounded in trust, flexibility, and local service. Whether you're shopping for your first vehicle or upgrading to something more reliable, partnering with a community bank can make all the difference.

Read Post

8/1/2025

Step-by-Step Guide to Applying for a Home Loan with Farmers Bank

Buying a home is one of life’s biggest milestones, and the home loan application process doesn’t have to be overwhelming. At Farmers Bank, we’re committed to helping you navigate every step with confidence and clarity. Whether you’re buying your first home or upgrading to your next, our mortgage guide will help you feel more prepared when applying for a loan.

8/1/2025

The Benefits of Refinancing Your Mortgage with Farmers Bank

If you’ve been in your home for a few years, there’s a good chance your financial situation, or the mortgage market, has changed. That’s why many homeowners explore mortgage refinancing as a way to improve their loan terms, reduce monthly payments, or access equity. At Farmers Bank, we make the refinancing process straightforward and personal, helping you unlock financial advantages that align with your goals.

8/1/2025

Advancing Agriculture: Loans for New Farmers

Starting your own farm is a bold and rewarding move, but it comes with a unique set of financial challenges. Whether you're purchasing your first acreage, investing in new equipment, or simply managing seasonal cash flow, having the right financial partner makes all the difference. That’s why Farmers Bank is proud to support Idaho’s agricultural community with a full suite of lending options designed specifically for new and growing farm operations.

7/3/2025

Fuel Business Expansion with Flexible Commercial Loans

As your business reaches new milestones, you may face opportunities that require significant capital, whether it’s opening a second location, purchasing high-value equipment, or scaling your operations to meet increased demand. That’s where commercial loans from Farmers Bank come in. These powerful financial tools are designed to help businesses like yours fuel long-term growth, improve efficiencies, and take bold steps forward.

7/3/2025

Financing Personal Dreams: Options with Personal Loans

Life is full of big moments, and sometimes those moments come with big price tags. Whether you’re renovating your home, paying for education, or finally making that dream purchase, personal loans can be a smart and flexible way to make it happen. At Farmers Bank, we offer customized solutions to help you finance life’s major expenses with confidence.

7/3/2025

Navigating SBA Loans: A Pathway to Business Success

For small business owners looking to grow, access to funding can often be the biggest hurdle. That’s where Small Business Administration (SBA) loans come in. Designed to make capital more accessible, SBA loans offer a powerful pathway to business success. At Farmers Bank, we’re proud to partner with local entrepreneurs by providing the support, tools, and financing they need to thrive.

Additional Articles:

December

- How to Leverage SBA Loans for Business Growth

- Home Equity Loans vs Home Mortgages: What’s Best for You?

November

October

August

July

June

- Tailoring Your Home Purchase: Mortgage Options at Farmers Bank(Opens in a new Window)

- Bridging Financial Gaps with Farmers Bank Ready Reserve (Opens in a new Window)

- Fueling Farm Operations: Comprehensive Agricultural Loans(Opens in a new Window)

May

April

- Unlocking Homeownership: Navigating Home Mortgage Loans with Farmers Bank(Opens in a new Window)

- Personalize Your Banking Experience with MyCardCreation®(Opens in a new Window)

March

January

12/03/2024

Mobile Banking Tips: How to Bank on the Go!

It has become more important than ever for people to be able to manage their finances while on the go. Mobile banking provides the convenience of accessing your accounts, making transactions, and monitoring expenses directly from your smartphone or tablet. Farmers Bank’s mobile banking app combines innovative features with secure online banking to ensure your finances are always at your fingertips.

12/02/2024

Securing Your Dreams: Home Loans and Mortgages in the Magic and Treasure Valley

Owning a home is one of life’s most significant milestones, and in Idaho’s Magic and Treasure Valleys, it’s a dream worth pursuing. At Farmers Bank, we’re here to make the journey to homeownership as smooth as possible with comprehensive home loans Idaho products, personalized mortgage services, and expert advice on navigating the real estate market.

12/01/2024

Business Bill Pay Solutions - Making Expense Management Easy

Managing business expenses effectively is critical for keeping your company running smoothly. Farmers Bank’s business bill pay solution is designed to simplify expense management, improve payment accuracy, and save valuable time for business owners. Whether you're managing invoices, approving payments, or setting up recurring transactions, our business bill pay tools put control back into your hands.

11/03/2024

Making the Most of Personal Check Cards and uChoose Rewards

Personal check cards are more than just an easy way to pay. They’re a portal to seamless transactions, greater financial control, and rewards that enhance the everyday banking experience. Farmers Bank has taken it a step further by adding uChoose Rewards to bring even more value to every swipe, tap, and online transaction. Dive into the exciting world of personal check cards and discover how uChoose Rewards can maximize the rewards in every transaction you make.

11/02/2024

A Tradition You Can Count On: The Philosophy Behind Our Exceptional Customer Service

Since 1917, Farmers Bank has been more than just a financial institution. Established in the heart of Idaho’s Magic Valley, our bank was founded on the timeless principles of banking trust, community focus, and an unwavering dedication to exceptional customer service. For over a century, we’ve remained a pillar of reliable banking Idaho residents rely on, upholding values rooted in integrity, respect, and a steadfast commitment to those we serve. Our story is one of resilience, devotion, and community.

11/01/2024

Exploring Personal Banking Options at Farmers Bank Idaho

When it comes to banking, having choices matters. Farmers Bank Idaho understands that each customer’s needs are unique, which is why they offer a range of personal banking services tailored to help you achieve your financial goals. From convenient checking accounts to interest-bearing savings and reliable credit card options, Farmers Bank Idaho makes managing your finances easier and more rewarding.

10/02/2024

Online Banking Services in Idaho: A New Era of Convenience

Digital banking has transformed the way we manage our finances, especially in rural areas like Idaho. Farmers Bank is at the forefront of this transformation, offering comprehensive online and mobile banking services that bring the bank to you, no matter where you are. With secure and user-friendly features, Farmers Bank ensures that your banking experience is not only convenient but also safe and reliable.

10/01/2024

Agricultural Loans in Idaho: The Farmer's Guide to Success

Agriculture is the backbone of Idaho's economy, and at Farmers Bank, we are committed to supporting our local farmers with tailored financial solutions. Whether you’re looking to expand your farm, invest in new equipment, or improve cash flow, our agricultural loans are designed to help your farming business thrive. This guide will provide an overview of the agricultural loans available, share success stories from local farmers, and offer tips on applying for financing that can make a difference for your agribusiness.

03/03/2024

Trusted Magic Valley Bank: Farmers Bank is your Financial Partner

Are you on the lookout for a reliable banking partner in Magic Valley to address your diverse financial needs? Your search ends here at Farmers Bank. With a steadfast dedication to providing tailored service and comprehensive solutions, we stand ready to accompany you on your financial journey in the Magic Valley.

03/02/2024

Find the Best Personal Checking Accounts for your Needs

When it comes to managing your money, finding the best personal checking accounts is key. These accounts are more than just a place to stash your cash; they're a crucial tool for everyday financial transactions and long-term planning. Mastering the art of identifying essential attributes such as minimal charges and seamless availability will significantly enhance your financial toolkit.

03/01/2024

Your Guide to Navigating Loans in Twin Falls

Finding the right loans Twin Falls and the Magic Valley can be a game-changer for many, whether it's to cover an unexpected expense or fund a significant purchase. Our objective is to illuminate the spectrum of borrowing avenues accessible, not only within Farmers Bank Twin Falls but also encompassing broader options. Navigating the application journey, we'll spotlight the essential paperwork and criteria you must meet.

Additional Articles:

December

November

October

- Online Banking Services in Idaho: A New Era of Convenience

- Agricultural Loans in Idaho: The Farmer's Guide to Success

March

2023 Blogs

December

November

- Empowering Farmers: One Agriculture Loan at a Time

- How to Choose the Best Home Equity Loan for Your Needs

- Understanding Idaho Mortgage Rates: Farmers Bank Offers Competitive Options

October

September

- Take Advantage of the Benefits of an ITM Near Me

- The Benefits of ACH for Business Owners and Customers